FHA Loan Limits Increase in 2022: Why It's Good for Homebuyers

Posted on Sep 10, 2021

Big news for FHA loans: the conforming loan limits are going up. This is good for homebuyers since...

Posted on Sep 10, 2021

In our last market outlook, we were lamenting the severe lack of homes to purchase relative to demand, and were hoping to see some inventory increase to provide relief to the extreme seller’s market conditions.

The good news is that we did see a small uptick of inventory over the summer in July, but the bad news is that we trended right back down again in August, and are seeing new record lows for the month’s supply of inventory in some markets.

Bottom line: interest rates are low and there aren’t enough homes to go around which is fueling a sustained, ultra-competitive housing market.

Each of our local markets has exhibited some variation of this pattern: home prices have appreciated rapidly over the past two years, and inventory is way down in comparison to pre-pandemic levels.

Philadelphia

Greater DC & Beltway

We saw 1-month inventory down from 1.2 in July, but this is up from an all-time low of 0.7 in March.

Greater Baltimore / Maryland

Orlando

Inventory is down to an all-time low of 0.8 month from 1.1 in July, and like other markets is still well below pre-pandemic levels of around 3 months of supply.

Tampa

Jacksonville

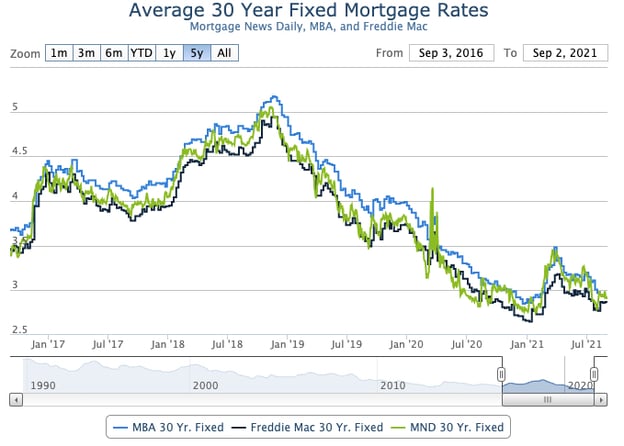

After spiking a bit from the all-time lows we saw earlier this year, the average 30 year fixed mortgage rate is trending back down. Nationally, rates climbed from the all-time low of 2.87% in Jan 2021 up to 3.42% in April 2021, and have from that point trended back to 2.93% and are seemingly continuing to drop.

We don’t know what the Fed will do, but between the Delta outbreak persisting and a weak August jobs report any “taper” seems unlikely and the low rates we are seeing are likely to persist or potentially even drop.

At this point it’s hard to expect any significant increase in inventory in the short term, though we did see a bit of a bounce in July and an uptick in average days on market in most of our regions, which signals a potential bit of softness to the current extreme levels.

So long as mortgage rates remain as low as they are now, homebuyers have an additional incentive to actively search – keeping competition high and reducing inventory.

If you’re in a position to buy and sell a home, now is still a prime time to do so. Despite the difficulties you may encounter as a buyer, you’re going to have two important factors working in your favor: extremely low-interest rates for your new home, and a strong seller’s market in which to sell your existing home.

If you’re selling a home, there are signs that competition is ebbing a bit when we compare late summer to early spring, so potential sellers who were on the fence may want to jump in now and cement their profit before we see an increase in average days on market and available inventory.

Subscribe to our newsletter to get essential real estate insights.

Posted on Sep 10, 2021

Big news for FHA loans: the conforming loan limits are going up. This is good for homebuyers since...

Posted on Sep 10, 2021

The housing market may have been nuts, but the rental market last year wasn't much better. Millions...

Posted on Sep 10, 2021

As millennials increasingly enter the housing market, a new question looms: can you buy a house...