How Much are Closing Costs in NJ? What You Should Expect to Pay

Posted on Jan 04, 2023

Homebuyers often save and save for their home’s down payment, only to realize when they talk to...

Posted on Jan 04, 2023

According to a recent Bankrate survey, about 20% of millennials are unhappy with their home purchases due to the unexpected costs of buying a home (like maintenance and repairs). If it’s your first time buying, you might be surprised at just how many hidden fees there are.

Research is key when it comes to figuring out how much you’ll need to spend in order to buy a house. Being prepared for potential costs ensures you're looking for homes within your true budget (one that accounts for the costs of maintenance).

Here’s what you need to know.

Closing costs are one of the biggest expenses that first-time home buyers are often unprepared for. In the U.S. closing costs average from 2% to 5% of the loan amount - so for a $500,000 home, that’s $10,000 to $25,000.

“Buyers often have no idea that there are even closing costs to begin with,” observes Orlando-based buyer agent Daniel Robinson. “Closing costs are quite detailed, and they are on an individual basis so it’s not like a one-size-fits-all price.”

.jpg?width=720&height=378&name=closing_costs-Jul-11-2023-09-32-17-5961-PM%20(1).jpg)

Looking at the U.S. average, though, isn’t a great barometer for what you’ll pay since closing costs vary greatly by state, as well as the house itself. In Indiana, for example, homeowners pay less than 1% of their home sale price in closing costs; in Delaware, homebuyers pay closer to 5%.

Closing costs cover a large variety of fees.

Here are the average prices for several common closing fees:

You want to estimate high for closing costs, since you’ll need to cover all these costs out of pocket. It’s also possible that you may have to pay certain costs twice. If a home inspection turns up an un-disclosed major issue, for example, you may not opt to move forward with the sale - which means you’ll lose the money you spent on the inspection.

Want to get an idea of what closing costs for your local area and budget will look like?

Most homebuyers have heard of the downpayment, but it’s worth noting since not everyone is familiar with the actual requirements. If you buy a home, your lender wants you to have some skin in the game to ensure you’re more likely to pay off the loan. Plus, putting money down reduces the interest you have to pay over time - saving you money.

Many people are surprised to learn that 20% down is no longer the standard - in fact, the average first time home buyer puts down 7%, while repeat buyers are putting down 17%.

The minimum you’ll need is 3% (with exceptions for VA and USDA loans).

“If you're doing the conventional loan you can put down as little as 5%, and if you’re a first-time home buyer in some cases you can put as little as 3% down, even conventionally,” explains senior mortgage advisor Casey Hansen.

Find out more: How Much to Put Down on a House: the Problems with 20%

The downside of putting less than 20% down on your mortgage is that it will trigger private mortgage insurance, or PMI.

The higher your credit score, the less you’ll need to pay in mortgage insurance. According to NerdWallet, a homebuyer with a credit score of 760+ buying a $350,000 home with a 10% down payment can expect a monthly PMI of $152 - and can expect to pay PMI for 7.4 years. After that point they’ll have 20% equity in their home, which will cancel the PMI.

PMI can often feel like a deterrent to buying a home, but it’s important to keep this number in perspective. $152 might feel like a lot, but if you opt to rent instead of buy, you’ll likely be paying many times that amount to a landlord - without building any equity.

If you’ve always paid rent to a landlord, property tax may come as a surprise - and it can be a hefty fee. Property tax is often rolled into the estimated cost of your monthly mortgage payment.

This is one reason why two same-price homes can have different monthly payments - a higher local tax rate can mean paying an extra $50 a month.

Keep in mind that property taxes are tied to the valuation of your property. With property values rising, so do your taxes.

According to The Washington Post, average property taxes increased 1.8% from 2020 to 2021, going from $3,719 to $3,785 (annually).

Renters aren’t always required to have insurance, but homeowners are. Your lender wants to know that if something happens to the home, you’ll be able to fix it. Like property taxes, this is a cost that’s rolled into your monthly mortgage payment estimate so it’s not going to be a total surprise.

According to Nerdwallet, the average cost of home insurance is $1,784 per year - but this number can vary depending on where you live, the size of your house, the scope of the coverage, and so on.

Don’t just go with the lowest price you can find: read reviews too. About 1 in every 20 homes have a claim filed each year, so the odds that you’ll eventually have to deal with your insurance are fairly high. You don’t want to get stuck dealing with the insurance company that takes two weeks to deal with a plumbing disaster that takes out your entire first floor.

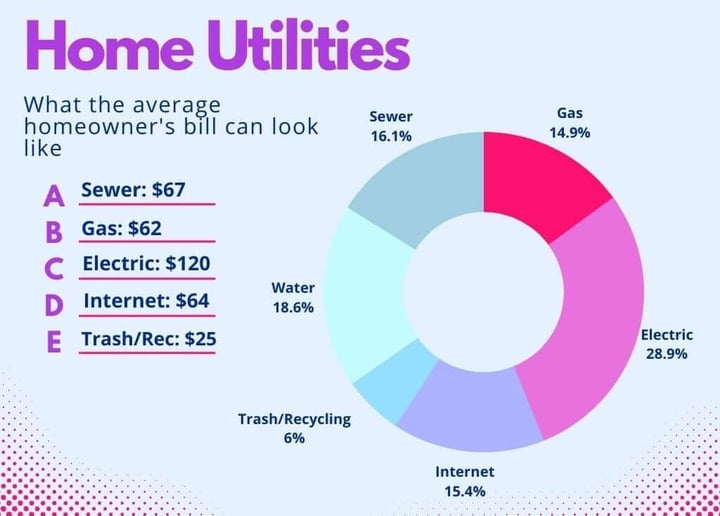

Most renters are familiar with paying utilities like electric, gas, and internet. Utilities like trash, sewer, recycling, and water, however, are often paid by the landlord and operate as an unseen cost. Even the utilities you were familiar with, though, might cost more if you’re transitioning from a one-bedroom apartment to a three-bedroom house.

Here are the average costs you can expect to pay per month:

When you’re your own landlord, you have to shoulder the costs of broken appliances yourself. It’s a good idea to set aside money every year for not only fixes and replacements, but also routine maintenance that helps extend the life of your appliances.

Some homebuyers opt to buy a one-year home warranty or they receive one as an incentive from the home seller. This can help mitigate unknown, large expenses as you adjust to your first year of homeownership.

Keep this in mind when you’re reviewing a potential home’s property disclosure and the listed appliances. A dishwasher that’s already 15 years old, for example, might not be around for too much longer.

When you have a landlord, it’s often possible to ask for a discount on the rent when you’re going through difficult times. Landlords can also allow tenants to pay the rent late. With a lender, though, there’s typically less wiggle room. For this reason it’s important to have a few months’ worth of mortgage payments saved in case something happens and you need to pay despite having lost your job or dealing with an illness or emergency.

Vanguard recommends having 3-6 months’ worth of expenses saved (not just mortgage payments, but food, utilities etc. as well). Foreclosure is a financially devastating experience and will stay on your credit score for 7 years if you have to go that route.

When was the last time you changed the air filter in your landlord’s HVAC system? For plenty of renters, the answer to this and other related maintenance questions would be “never.” Understandably, renters don’t typically want to invest in their landlord’s house - especially if they only plan on being there a couple years.

Once you own a house, though, you have an incentive to keep it well maintained. You’ll reduce the likelihood of expensive fixes, and helping it maintain value until you’re ready to sell.

Maintenance tasks that you might not bother with as a renter, but should as a homeowner, include:

Costs will vary depending on whether you hire someone or do it yourself, but you can often purchase enough air filters for the year for $20 or less from stores like Home Depot.

For more info check out: Property Maintenance for Your New Home

If you want to have a great home owning experience, reading up on the hidden costs and fees of buying a house is essential. Preparing your finances will help you stay in front of unexpected issues, ensuring that they remain resolvable problems rather than financially devastating issues.

Want to learn more about buying a house? Check out our 5 Step Home Buying Guide

Subscribe to our newsletter to get essential real estate insights.

Posted on Jan 04, 2023

Homebuyers often save and save for their home’s down payment, only to realize when they talk to...

Posted on Jan 04, 2023

First-time homebuyers are often shocked to hear that after all the saving they did for the down...

Posted on Jan 04, 2023

First-time homebuyers will often save and save for the down payment for their home, but all too...