Closing Costs in Virginia: What Homebuyers Need to Know

Posted on Jul 20, 2021

First-time homebuyers are often shocked to hear that after all the saving they did for the down...

Posted on Jul 20, 2021

The old adage for buying a home has always been “put 20% down” - in other words, be ready to fork over 20% of your home’s selling price at the closing table as a down payment. More and more, though, potential homeowners are realizing that not only is 20% unnecessary - sometimes, it can even work against you.

Is putting down 10%, or even 5% on a house bad? Here’s what you need to know.

One of the biggest benefits of putting 20% down is lower monthly mortgage payments. Since you pay more upfront, you logically need to borrow less - and you'll pay less in interest fees over time.

If you opt for 5% down on a $600,000 home, you need to pay back $570,000 plus interest on $570k. If you opt for 20% down on a $600,000 home, you only need to pay back $480,000 plus interest on $480k.

When you put down 20% you also avoid PMI (private mortgage insurance) which will otherwise be an additional monthly bill. As a result of fewer bills, you'll typically have more purchasing power with a higher down payment, and can afford a more expensive home.

The problem with 20% nowadays is that it can take people years to save up enough money. The average home price today is $440,300, which means potential homeowners would need to save up $88,000 to cover a 20% down payment - and enough to cover closing costs (which amount to many thousands of dollars).

Say it takes you three years to save that money. Three years ago, the average American home was $322,500 (Source: Fred Economic Data). Someone who waited that 3-year period to save up and just bought a home today lost out on an average of $117,800 in appreciated value.

Of course, homes appreciated incredibly quickly over the past three years - we're unlikely to see such rapid appreciation gains again now that the mortgage rate has gone up. Regardless, though, home prices in the U.S. do steadily appreciate over time for the most part - so you can see that there is a true price to waiting while saving.

Why is 20% given as advice? Because it used to make more sense. When homebuyers used to put 20% down on a home, home prices were more aligned with wages. Gains in home prices have consistently outpaced income average income gains in the U.S.

Finally, it's worth considering where your money goes while you wait to buy. The money you're paying in rent during that time that could be put towards your own equity. Effectively, you’re paying off someone else’s mortgage instead of your own.

Many people are wary of taking on loans. While this is a prudent outlook, it’s worth keeping in mind that not all borrowing is bad. In fact, borrowing can help you leverage your money when you need it most. How?

Right now, mortgage rates are still on the low end historically, despite raises by the Fed. It’s worth considering whether you should be tying up your money in your home - even if you can put 20% down.

According to Nerdwallet, the average stock market return has been about 10% per year for nearly the last 100 years (not accounting for inflation). Historically (not just looking at the anomaly of the 2021), homes appreciate 3.8% per year. In other words: although there is no guarantee (and this is not financial advice), a homeowner could opt to buy a home now, and put the money they would have saved up for a down payment into the stock market - thus minimizing some of the loss that comes with taking on more debt.

In 2019, the National Association of Realtors found that the typical down payment on a house or condo was just 12% down. For first-time homebuyers, that number drops to 6% down. In other words, putting down less than 20% on your home is far more common than you might have thought.

If you decide that owning a home is your priority, rather than having 20% down, you have a few different options. With a traditional lender, many homeowners can make a down payment of as little as 5%, and first-time homeowner loan programs (like the FHA) can bring that percentage down to as low as 3.5%.

“If you're doing the conventional loan you can put down as little as 5%, and if you’re a first-time home buyer in some cases you can put as little as 3% down, even conventionally,” explains mortgage advisor Casey Hansen.

If you’re buying a $400,000 home:

Keep in mind that in addition to putting money down, you’ll also be expected to cover closing costs - and you typically will be paying for those upfront, without the option of rolling them into your loan.

When homebuyers opt for a downpayment of less than 20%, they typically need to pay for PMI (private mortgage insurance).

To summarize from our guide to PMI:

While many potential homeowners hate the idea of paying extra insurance for their mortgage, what they should really do is look at the numbers.

“Some people don’t want to have to pay PMI. it’s viewed as wasted money that’s thrown away. But in reality, it’s not wasted money, it allows you to buy a house for less than 20% down,” notes Hansen.

The actual monthly cost of PMI will vary based on numerous factors including the loan amount, your down payment, and your credit score, but for many homeowners it ends up being under $100 per month - and recall, you can get rid of your PMI once you reach 20% equity in your home.

“Each situation is pretty unique to the borrower and things like credit score, property type, down payment, and other variables can impact the cost of PMI,” notes Hansen. “If you're talking about a government loan, like an FHA loan, it’s a little different - it’s called MI (mortgage insurance), and then it’s a flat amount regardless of any criteria. Doesn't matter how good your credit is, it’s just going to be a flat amount.”

And as we’ve noted in our complete guide to PMI, FHA’s MI does not go away when you reach 20% equity in your home.

“A lot of times people have 20% to put down, but they might just barely have enough to put down 20%. And usually, if someone has good or excellent credit, the PMI costs have come down pretty substantially these last couple of years,” he notes. “In many cases, once people find out what the cost is, they decide to put down less than 20%. In some cases, people have more than 20% to put down and they still decide they’d rather hold onto the cash for different reasons.”

Ultimately, the homeowners who opted for PMI three years ago when the market wasn’t as hot are in a great position today. They were able to buy a home before things got super competitive and according to Zillow, “Home values have gone up 13.2% over the past year and Zillow predicts they will rise 14.9% in the next year.” As a result, many of them will already have enough equity in their home to eliminate the PMI.

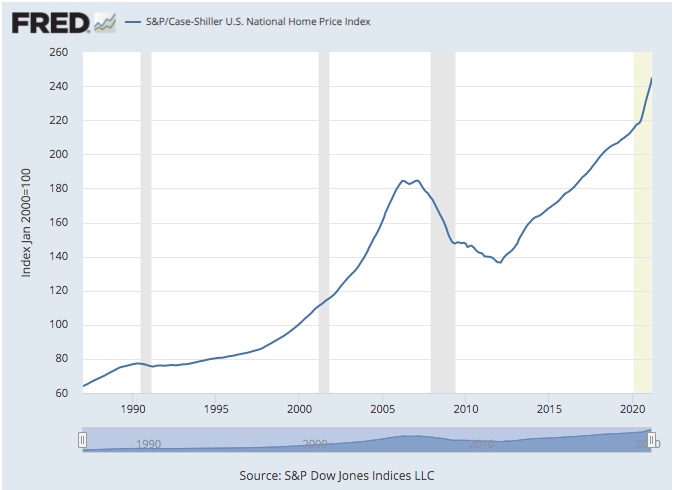

The market has been especially hot this year, and there’s no guarantee that home prices will continue to rise at such a rapid pace. However, over the past several decades one can observe that, even though there’s been a few dips, home prices have steadily appreciated over time.

Source: FRED

There's no right or wrong answer to putting 20% down on your home, and there are benefits to both approaches.

If you put down less than 20%:

If you put down 20% (or more):

Subscribe to our newsletter to get essential real estate insights.

Posted on Jul 20, 2021

First-time homebuyers are often shocked to hear that after all the saving they did for the down...

Posted on Jul 20, 2021

If closing costs have caught you by surprise, you wouldn't be the first. First-time DC homebuyers...

Posted on Jul 20, 2021

Over the past several years, the average cost of buying a home has skyrocketed in most areas of the...