Are Home Prices Dropping in 2024? What the Data Shows

Posted on Jul 21, 2022

Note: This article is a rewrite from 2023, updated for current market conditions. Are home prices...

Posted on Jul 21, 2022

A looming recession, inflation, and rising mortgage rates have made plenty of homebuyers wary of entering the market. According to a recent National Housing Survey, only 20% of consumers believe it’s a good time to buy a home. Some potential buyers wonder if falling home prices are on the horizon - and whether it makes sense to wait.

There are benefits and drawbacks to buying a home while the market is in flux: here's what you need to know.

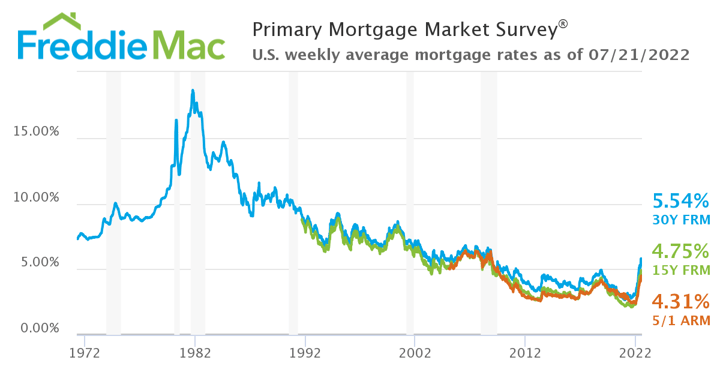

Mortgage rates rose rapidly this year as the Fed looked for ways to tamp down inflation. After reaching historic lows of under 3% last year, average 30-year rates are now closer to 6%. When the rates were low, buyers eager to take advantage of cheap borrowing flooded the market. Now that rates have risen, many buyers have backed off as they saw their estimated monthly mortgage payments jump by hundreds of dollars.

But there are a few reasons that rising interest rates aren’t as bad as they seem.

Of course, it’s going to sting to see mortgage rates rise from a record low of 2.7% to 6.4% where they are now (and perhaps higher as the year progresses). This dramatic jump means that homebuyers have to cope with a more limited budget, and larger, newer homes in desirable neighborhoods are further out of reach.

In context, though, mortgage rates today are low. In 1980, you would’ve been paying close to 15% for a 30-year mortgage, and in 1990, the rate hovered around 10%. The overall average since 1971 has been 7.77%, according to The Mortgage Reports. Perspective is key when it comes to evaluating the current mortgage rate.

Second, rates are not set in stone the way home prices are. If you stay in your home for the entirety of the 30-year term, there’s a fair chance that mortgage rates will dip again. If they do, you always have the option of refinancing your loan in order to take advantage of the lower rate. Although refinancing does come with a processing fee, it can often save homeowners thousands of dollars overall.

Homebuyers also have the option of doing an Adjustable Rate Mortgage. Though these got a bad rap during the last housing crisis, they can actually be a useful way to receive a lower rate - especially if you don't plan on living in your house for the entire 30-year term.

Third, mortgage rates and home prices tend to work like a balancing scale. When one goes up, the other goes down. With fewer people seeking to buy homes, competition eases - leading to fewer bidding wars that drive prices sky high, and more pressure on sellers to accept reasonable offers.

Fourth, many homebuyers are asking: will rates fall again, allowing for cheaper borrowing in 2023? According to Business Insider, experts believe rates aren't likely to drop again until the end of 2023 or into 2024. And even then, you shouldn't bet on rates reaching those historic lows again.

Make no mistake: homeowners are definitely paying more in interest now and will have to adjust their budgets accordingly. Rising interest rates aren't easy to deal with. But when it comes to whether or not waiting to buy a home makes sense - waiting won't bring back the historically-low rates that were an anomaly.

"Even with interest rates constantly fluctuating, being able to buy a home is always a financially smart decision," notes Maryland-based buyer agent Daniel Neves.

Sellers realize that the window for maximizing their profits is closing. As they watch listing after listing in their local area do price reductions to the tune of several thousand dollars, more and more sellers have been entering the market in an attempt to get in before the hot market dissipates completely.

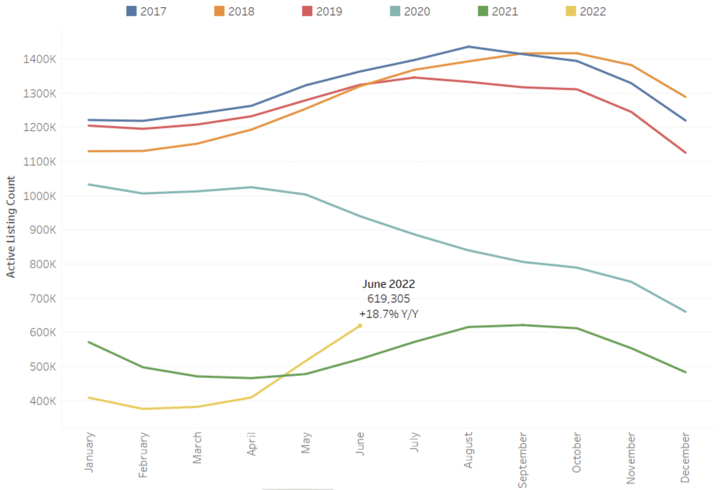

In June, Realtor noted that there was YoY inventory growth for the first time since mid-2019, with the market seeing a 6.3% increase in newly listed homes since last year. And according to the National Association of Realtors (NAR), "The inventory of unsold existing homes rose to 1.26 million by the end of June, or the equivalent of 3.0 months at the current monthly sales pace."

This is big news, because the incredibly low inventory of homes on market has been a major driver of rising prices. The increase in inventory gives buyers more options - and more leverage. Home value gains will be much more modest now that sellers are receiving one or two offers in many cases, not 20.

"An example of this shifting market: we were able to win an offer for our buyer $30,000 below the asking price with seller help recently," notes Neves. "It wasn't like this a year ago. Before, buyers would have very little to no say in negotiations, but now with the market shifting, buyers have some leverage on sellers who want to overprice their home."

National inventory is trending upward, and that's been true in Houwzer's local markets as well. While that bodes well for homebuyers today, one benefit of waiting until 2023 is the potential for an even greater shift in inventory, which could put more power in the hands of buyers.

Although inventory is slowly rising, it’s still far below the 6-month supply which indicates a balanced market (Washington DC's supply of housing inventory rose 20% in June YoY, for example, but that only took it from 1 month to 1.2 months' supply). Make no mistake, it will still be a seller’s market for the next several months, if not several years.

Buyers today, though, should feel more comfortable and confident when it comes to asking for home inspection and financing contingencies - the likes of which were tough to come by in 2021’s crazy market conditions.

"In my local area I am seeing some changes. Some pockets of homes are staying on the market a little longer, with prices of homes going down - a year ago or during COVID times, they would have easily sold for asking price and been on the market less than week," observes Neves.

If you're not buying a house, there's a good chance you're renting in the interim. Unfortunately, there is no hiding from rising housing costs. Even if you decide to rent instead of buy for another year or two, rental prices have skyrocketed around the country. On average rent rose 11% last year, and some metro areas experienced average rental increases of up to 40%.

While buying a home might be a costly endeavor in the short term, in the long term it sets you up with predictable expenses and a hedge against inflation. Even though rent will continue to rise year by year, your mortgage payment will increase more gradually (the actual amount you pay to the lender is pre-determined if you have a set rate - but property taxes will go up in time).

And of course, when you pay rent, you ultimately pay off your landlord's mortgage. When you pay for your home, that's equity toward your future.

Let's say your current monthly rent is $1,200, and your estimated monthly mortgage payment is $1,500. If you do the math too quickly, it might seem like you "save" $300 per month by continuing to rent - and this can be tempting. But at the end of the rental year, you net $0 from all those payments.

On the other hand, if you buy your home? By the time a full year rolls around, you'll have already paid $18,000 toward your home loan balance - and you don't need to worry about your landlord hiking your rent by $500 because "that's the market value now."

Many potential home buyers are asking themselves whether it’s a good idea to wait until 2023 to buy a home, or whether it's better to buy a home now. There are benefits and drawbacks to both approaches.

If you buy a home in 2023, you get more time to save for a down payment, which might help to lower your monthly payment once you get a mortgage. You may also benefit from a further increase in housing inventory, which means more choices and fewer bidding wars that drive up prices. And if you haven't quite figured out a 5-year plan (which is advisable when you buy property), waiting until 2023 buys you additional time to figure things out. Not everyone is in the right situation yet to buy a home - and that's okay!

On the other hand, home prices are expected to continue rising - just at a less blistering pace. CoreLogic is predicting an increase of 5.6% in average home prices over the next year. If this holds true, a $400,000 home today will cost approximately $422,400 a year from now (which may negate any money you save while waiting).

Additionally, you miss out on the benefits of owning a home today (not having to answer to a landlord, building your equity, avoiding crushing lease increases).

Regardless of whether you plan to buy a home now or in 2023, don't bank on dramatic price reductions à la 2008.

"Homebuyers waiting for a market crash will be disappointed. Today's market is different from the Great Recession housing bubble, as supply and demand are the driving forces behind home prices - and lenders follow more stringent guidelines today for loan approvals," explains Neves. "But now as we see a slow shift in the market, the competition for buying a home is going down."

Ready to start the process of buying a home?

Subscribe to our newsletter to get essential real estate insights.

Posted on Jul 21, 2022

Note: This article is a rewrite from 2023, updated for current market conditions. Are home prices...

Posted on Jul 21, 2022

Mortgage rates have been on a journey this year - and it’s the sort of journey that makes buyers...

Posted on Jul 21, 2022

Head to our more recent post: Should I Buy a House in Spring 2023 or Wait?