Philadelphia Inventory Remains Stubbornly Low, But Buyers Are As Determined As Ever

Posted on Mar 23, 2022

Houwzer’s Senior Economic Advisor, Kevin Gillen, has released the Philadelphia housing market...

Posted on Mar 23, 2022

Home prices rose so rapidly in 2021 that many potential homebuyers are now wondering if the pendulum will swing in the other direction. Will home prices drop in 2022? Unfortunately, the opposite is more likely. Here are 5 reasons why home prices will keep going up in 2022.

Understanding why housing prices are going up helps clarify why home prices aren’t dropping. One thing to keep in mind is that a driving force behind housing demand is the creation of new households, which follow population growth.

More households have been forming than dissolving over the past decade. About 12 million additional households formed over this period, while only 7 million new single-family homes were built. And during this time, the U.S. population grew by 19.5 million people (+6.3%).

Keep in mind that the five largest birth years for millennials (1989-1993) are all hitting 30 years old right now - a significant age milestone that is often tied to seeking homeownership.

A related trend to pay attention to is the rising number of “solo households.” It’s becoming more normal in the U.S. to get married later in life, or to never couple up at all - or to de-couple, as a large number of baby boomers have done. As a result, according to the 2020 Current Population Survey, 36.1 million households—or 28% of all households—are sole-person. This number has more than doubled in the past 40 years. More solo households, though, represent an even greater crunch on the housing market as each person looks for their own home, rather than sharing one with a partner.

When the 2007/08 housing crash happened, it did more than just stall the economy for years. New home building - both multi-family dwellings and single-family residences - dramatically fell off after the crisis, and only very recently have building starts been catching up to pre-recession levels.

There are a few reasons for this. There are more regulations on buildings than there used to be. According to the National Association of Home Builders, the latest estimates show that government regulations account for 24% of the final price of a new single-family home.

Material costs have also gone up - especially during the pandemic. Material costs for residential construction rose 15% in 2021, according to the Bureau of Labor Statistics’ Producer price indexes. Many of last year’s supply chain issues still haven’t let up, and might continue now that there is widespread trade conflict and rising fuel prices due to the Russian invasion of Ukraine (of relevance: Russia supplies roughly 10% of the U.S.’s hardwood plywood).

Because homes are so expensive to build right now, developers often favor building luxury homes and luxury buildings. Why? In a seller’s market, they’re going to have buyers lined up no matter what - due to the lack of other choices - and it’s easier to make a profit off of more expensive homes. There’s just not much incentive right now to build more affordable starter homes.

Zoning laws have also forced developers to run with a “work with what you got” mentality. Even if building a multi-family unit would create more affordable housing, developers are often held back by zoning laws specifying that only single-family homes can be built in areas designated for single-family homes.

If more homes were coming to the market, there would be less competition for those homes - so part of the basic problem is the persistent low inventory. If you thought this might improve in 2022, think again: so far, housing inventory in the U.S. has been reaching new lows.

Why is inventory so low? It’s a complex web of factors - some of which have already been outlined here.

We’ve noted the increased number of millennials looking to buy a home now that they’re reaching more of their earning potential. Historically as younger people look for starter homes, older generations have downsized in retirement and put their homes up for sale, freeing needed housing stock. Today, however, many baby boomers (who own 44% of the country's housing stock) are opting to age in place and make updates to their existing homes rather than move to a new one/to a retirement home/into their children’s home.

Another problem - for potential home sellers of all ages - is that the incredibly hot market has created a bit of a Catch 22 for sellers who need to buy their next home. While they might get a lot of competition and profits for their current home, they then have to enter this same cutthroat environment to buy - and in a time when contingencies are hard to come by. Many sellers are simply opting to wait so that they don’t get stuck selling their current home before they have their next one lined up.

Houwzer’s new Buy Before You Sell program helps sellers move on from their existing homes. Sellers can buy their next home in cash with Houwzer’s funds - then sell their current home for maximum profit. Selling later allows sellers to avoid the risk of getting stuck without a home and the complications of contingent offers.

As the cost of housing and the demand for rentals increased, Wall Street sharks sensed an opportunity. In 2021, investors bought nearly one in seven homes sold in America’s top metropolitan areas, according to The Washington Post and data via Redfin. And in the final three months of 2021, a feeding frenzy took place, with investors buying up 15% of all homes for sale. This is a notable increase, even rising above the investment levels that occurred pre-housing crash.

Investors have big pockets and don’t have to deal with the same lender/appraisal constraints as the average home buyer. Instead, investors can pay a premium upfront - knowing that they’ll make their profit back through renting out the property at a higher price.

It’s unfortunate that Americans are paying the price, but it’s part of the housing market landscape right now.

Interest rates have been at historic lows over the past year, meaning that buyers could afford more house with less money. With every one-point increase, the average buyer loses 11% of their buying power.

So when interest rates dipped, millions of would-be homebuyers were ready to buy a home no matter what it took - because they realized that even if they paid over asking, they would still be able to afford a nicer house than before.

Although mortgage rates have been slowly rising in 2022 - and will likely help temper the crazy highs of the housing market - they're still relatively low compared to rates over the past several decades. As potential homebuyers watch rates continue to rise, they may spend 2022 trying to get into a house before they go even higher.

It’s impossible to give an exact timeline for the emergence of a more balanced market, or even a buyer’s market where buyers have the upper hand in negotiations. As you can see, there are many different factors at play impacting demand and scarcity. There are also emerging technologies - such as 3D printed homes - that could impact the affordability of modern housing in ways we're not yet experiencing.

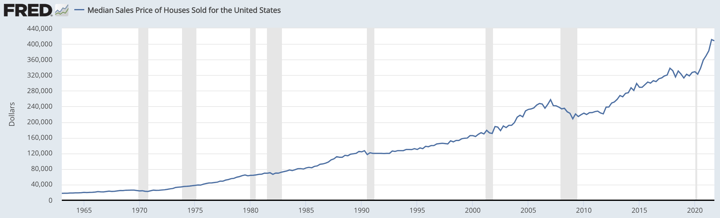

It’s worth noting that historical data doesn’t really support the idea of a dramatic drop in average price. The 2008 housing crisis shaped how many Americans view the housing market, and yet it was more of an anomaly event than something that should be expected to occur over and over.

As Should I Buy a House in 2022? The Answer, Surprisingly, Is Yes explains, you shouldn’t try to time the market. Even experts struggle to accurately predict the highs and lows of the housing market - and while you wait, you’ll continue to pay off someone else’s rent or be stuck in a home that doesn’t suit your current/future needs.

Rather than worrying over the question of “will housing prices go down,” instead, do the math and see whether buying a home today fits your long-term financial and life goals.

Subscribe to our newsletter to get essential real estate insights.

Posted on Mar 23, 2022

Houwzer’s Senior Economic Advisor, Kevin Gillen, has released the Philadelphia housing market...

Posted on Mar 23, 2022

According to data released by Zillow, U.S. home prices rose 13.2% over the past year. Fewer homes...

Posted on Mar 23, 2022

Note: This article is a rewrite from 2023, updated for current market conditions. Are home prices...