So you spotted a Zillow pre-foreclosure listing and you’re wondering what it actually means — and whether you can buy it. Here’s the honest answer. Maybe you’ve found the perfect home on Zillow – it’s the right neighborhood and the right size – and you’ve noticed that it says the home is in “pre-foreclosure.” You’ve probably heard about foreclosure, but what does pre-foreclosure mean – and does it present additional challenges if you want to buy the house? Here’s what you need to know.

What Does Pre-Foreclosure Mean on Zillow?

A pre-foreclosed home on Zillow is a home that has been already served a Notice of Default or lis pendens by the lender, but hasn’t yet been sold at a foreclosure auction. In other words, the homeowner probably missed at least three mortgage payments, but still owns the home.

While the home is slated for foreclosure, two other things could happen: the homeowner could pay off their debt and get back on track with their mortgage, or they can sell the home. Once a home is foreclosed, though, that means it’s been repossessed by the lender and can no longer be sold by the original homeowner.

It’s worth noting that if a home is listed as “pre-foreclosure” on Zillow, it just means that the home has been served a notice of default by the lender at some point in the past. That may have been months ago, and the home has since been sold to a buyer or gone to auction. In other words, this section isn’t always updated.

“Pre-foreclosed homes are not for sale at all. The prices that show somewhere on the listing are usually just the Zillow Zestimates – not a price the owner, a Realtor or bank came up with – and the pre-foreclosure status just means that at some point in history, there was a default notice mailed to the owner. It could be eight years ago, it could be current,” explains Lisa Armellino, a buyer agent based in the Philadelphia suburbs. “So the moment that that notice goes out, it becomes public record, and on Zillow it will become a preforeclosure listing.”

If you’re wondering how to check on the status of the pre-foreclosed home you’ve found, Armellino says it’s possible to do this on your own.

“I just go and look it up in the public record on the county site and see if anything is currently against the property or currently defaulted, and I’ll usually find out it happened years ago. I don’t know why Zillow keeps listing them,” she explains.

How Do You Find a Pre-foreclosure Home?

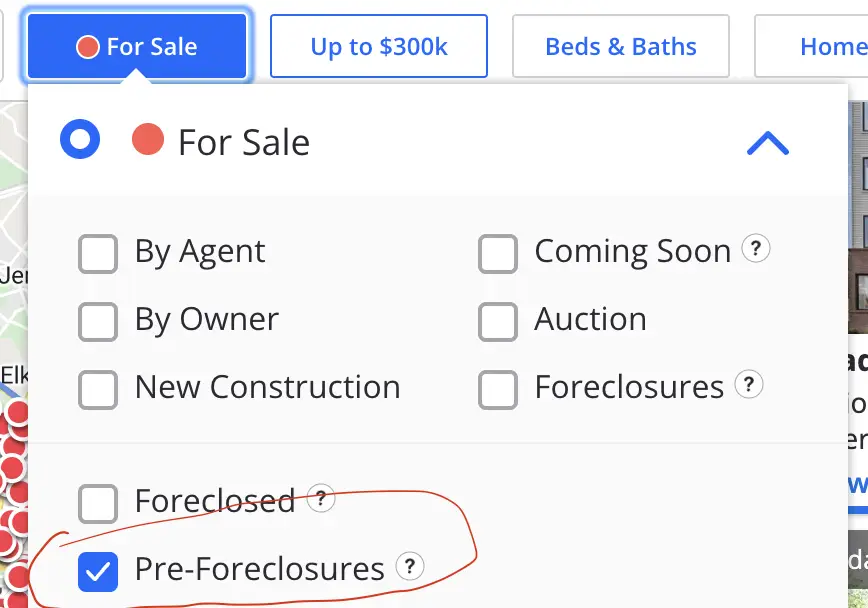

Zillow is one of the easiest online directories to find pre-foreclosure homes. You can use Zillow’s filters to specify only pre-foreclosed homes (make sure to un-check “foreclosed”).

Another way to find preforeclosure listings is in the public records section of your county recorder’s website. The terms to look for are “notice of default,” “lis pendens” and “notice of sale.”

How to Buy a House in Pre-Foreclosure

In order to buy a pre-foreclosed home, you would be working with the buyer to resolve their existing debt.

To get the ball rolling, you’ll need to get in touch with the homeowner. Although door knocking is likely the most direct route, keep in mind that they may not have any desire to sell – and they may find your presence intrusive as well. Prepare to be empathetic to their situation.

Disadvantages

Generally speaking, this process is easier if you decide to pay cash, because your lender will have a variety of rules and requirements that might make it difficult to purchase a home that is close to being in foreclosure. It can be quite difficult to get permission from the homeowner’s lender to buy a pre-foreclosed home as well.

“The problem is there’s already a default notice – you run into issues on Title when you are selling the house and you do actually need the bank’s approval. So it can be a harder transaction. For 1 in 50 properties, it might work out – maybe. But the rest of them, those are people still living in the house, and the notice might not even be current,” Armellino explains.

Another downside: buying a pre-foreclosed house is similar to buying a home in foreclosure – you’re buying it “as is” and you’ll need to cover the cost of whatever repairs are needed, as the seller does not have the financial means to do it themselves. Because the seller has likely been in financial trouble for some time, you should assume there’s a good chance that certain required/routine maintenance hasn’t been done – so immediate fixes might be required to make the home habitable.

It’s also not uncommon for pre-foreclosed homes to carry liens on them, as well as unpaid taxes – which you’d be responsible for covering. For this reason, buying a pre-foreclosed home is not a great idea for first-time buyers who are new to navigating the ins and outs of a home purchase and homeownership.

Advantages

The benefit to buying a pre-foreclosure home is that you can potentially get the home at a discount. You’ll need to pay off the homeowner’s existing debt – whatever’s left of their mortgage, any unpaid taxes, etc – but the rest is negotiable. You’ll also have less competition for the home than you would if it actually went to auction as a foreclosed home, which can help keep the price down.

And although the title search might present a challenge, some people do manage to buy a pre-foreclosure home with a conventional mortgage. If you get past the bumps, it’s just like buying any home on the market – you submit an offer, and they accept it (hopefully). This is a plus for many homebuyers, because homes that actually foreclose can’t be purchased with conventional home loans. So to prepare, you’ll definitely want to get a pre-approval letter from your lender before talking to the homebuyer or making an offer. A pre-approval letter is not tied to a specific home, it just says that you’re financially qualified to buy a home (up to a certain amount).

According to Street Directory, pre-foreclosures usually come in 20-50% below market value (though in this hot market, you might see smaller gains due to increased competition). The seller is incentivized to sell their home as fast as possible so that they can recoup at least some of their money, as well as avoid the negative impact a foreclosure would have on their credit score and future home-owning prospects.

So: Will that Zillow Preforeclosure Home Be Yours?

A pre-foreclosed home can represent a discount off the market value of a home – and after home prices skyrocketed an average of 20% over the last year alone, some homebuyers will see this as a huge benefit.

However, keep in mind that there are certain risks that come with a pre-foreclosed home – and it will be a smaller pool of homes available, so it’s unlikely that you’ll be able to find one in your ideal neighborhood. It may also be challenging to find a homeowner willing to sell to you in the first place.

If you haven’t already met with a Realtor and mortgage advisor, set up a meeting – you might not realize all your options for homes, as well as the various options there are for structuring a loan so as to lower the monthly mortgage payment. You might have more choices than you think!

(it’s free and comes with no obligation!)

How the Pre-Foreclosure Process Works

A Zillow pre-foreclosure label means the owner has missed mortgage payments and the lender has filed a notice of default, but the home has not yet been sold at a foreclosure auction. In other words, a Zillow pre-foreclosure is a warning stage, not a listing — the owner still controls the property and may catch up on payments, sell, or be foreclosed on.

That status is exactly why a Zillow pre-foreclosure can be confusing: the home isn’t officially for sale just because Zillow flags it. Reaching the owner, confirming their intentions, and moving quickly are what separate buyers who succeed from those who waste months chasing a Zillow pre-foreclosure that was never available.

Risks of Buying a Zillow Pre-Foreclosure

Pre-foreclosure deals can come with liens, deferred maintenance, or owners who simply aren’t ready to sell. Before you pursue a Zillow pre-foreclosure, budget for a title search and inspection, and be prepared for an emotional negotiation with a homeowner in financial distress. A good agent who has handled distressed sales is worth their weight here.

How to Buy a Zillow Pre-Foreclosure, Step by Step

If you’ve decided a Zillow pre-foreclosure is worth pursuing, having a process keeps you from spinning your wheels. Here’s the realistic path most successful buyers of a Zillow pre-foreclosure follow.

1. Confirm the status. Cross-check the Zillow pre-foreclosure flag against county records. The notice of default tells you how far along the process is and how much time the owner has.

2. Reach the owner. A Zillow pre-foreclosure isn’t listed, so you (or your agent) need to contact the homeowner directly and gauge whether they want to sell before the auction.

3. Line up financing. Sellers in distress need certainty. Pre-approval — or proof of funds — makes your offer on a Zillow pre-foreclosure far more credible than a tentative buyer’s.

4. Do your due diligence. Order a title search and inspection. Liens and repairs are common on a Zillow pre-foreclosure, and they can turn a “deal” into a money pit.

5. Negotiate and close. Work with the owner and their lender to agree on a price that clears what’s owed. Move quickly — a Zillow pre-foreclosure can flip to a bank-owned auction if the clock runs out.

Pre-Foreclosure vs. Foreclosure vs. Short Sale

It helps to know where a Zillow pre-foreclosure sits among distressed-property types. Pre-foreclosure means the owner is behind but still owns the home — this is the Zillow pre-foreclosure stage. Foreclosure means the lender has taken the property and is selling it, often at auction. A short sale is when the owner sells for less than they owe with lender approval. Each has different timelines and risks, and a Zillow pre-foreclosure generally gives you the most room to negotiate directly with a motivated owner.

Common Mistakes When Chasing a Zillow Pre-Foreclosure

Plenty of buyers get excited by a Zillow pre-foreclosure and then lose time — or money — on avoidable errors. Knowing the traps ahead of time keeps your search efficient.

Assuming it’s for sale. The single biggest mistake is treating a Zillow pre-foreclosure like a normal listing. It isn’t. The owner hasn’t necessarily agreed to sell, so your first job is outreach, not an offer.

Skipping the title check. A Zillow pre-foreclosure can carry second mortgages, tax liens, or HOA debt. Buying without a title search can mean inheriting obligations that erase your discount.

Lowballing a distressed owner. Owners in pre-foreclosure are stressed, not desperate to be insulted. A fair, fast, well-documented offer wins more Zillow pre-foreclosure deals than an aggressive one.

Moving too slowly. The foreclosure clock is always ticking. If you dawdle, the Zillow pre-foreclosure you wanted can be auctioned out from under you before you ever submit paperwork.

Going it alone. Distressed transactions have moving parts most buyers never see. An agent and a real estate attorney familiar with pre-foreclosure deals protect you from costly surprises and keep the timeline on track.

Should you wait for the foreclosure auction instead?

Sometimes waiting for the auction gets a lower price, but auctions usually require all cash, offer no inspection, and carry more risk. For most owner-occupant buyers, negotiating a Zillow pre-foreclosure directly with the owner is the safer route to a livable home at a fair price.

Zillow Pre-Foreclosure Timing and Financing Questions

How long does a pre-foreclosure last?

It varies by state and lender, but a Zillow pre-foreclosure typically runs anywhere from a few months to over a year between the notice of default and the foreclosure auction. Judicial-foreclosure states tend to take longer, which can give a buyer more time to negotiate a Zillow pre-foreclosure purchase.

Can the owner stop a pre-foreclosure?

Yes. An owner can cure the default by catching up on payments, refinancing, or working out a loan modification — any of which removes the Zillow pre-foreclosure status. That’s why you should never count on a Zillow pre-foreclosure being available until the owner has actually agreed to sell.

Do you need cash to buy a pre-foreclosure?

Not necessarily. Unlike an auction, a negotiated Zillow pre-foreclosure sale can often be financed with a normal mortgage, provided the title is clear and the home appraises. Cash simply makes your offer more competitive and your close faster.

Will buying a pre-foreclosure hurt the previous owner?

A fair Zillow pre-foreclosure sale can actually help the owner avoid a full foreclosure on their credit. Approaching the situation with empathy — and a clean, fast offer — is both the decent and the effective way to win the deal.

Key Takeaways: Buying a Zillow Pre-Foreclosure

- A Zillow pre-foreclosure is a status flag, not a listing — the owner still controls the home.

- You can buy a Zillow pre-foreclosure, but you must contact the owner and act before the auction.

- Budget for a title search and inspection; a Zillow pre-foreclosure often carries liens or deferred upkeep.

- An agent experienced with distressed sales dramatically improves your odds on a Zillow pre-foreclosure.

Zillow Pre-Foreclosure FAQ

What does pre-foreclosure mean on Zillow?

It means the homeowner has fallen behind on mortgage payments and received a notice of default, but the home hasn’t been sold at auction yet. A Zillow pre-foreclosure is a status flag, not an active listing.

Can you buy a house in pre-foreclosure?

Sometimes. You’d need to contact the owner (or their agent) directly and negotiate a sale before the foreclosure completes. Many Zillow pre-foreclosure homes never actually become available.

How do you find pre-foreclosure homes?

Zillow’s pre-foreclosure filter, county public records, and an agent with access to distressed-property data are the main routes. Expect to do outreach rather than simply make an offer.

Is buying a Zillow pre-foreclosure a good idea?

It can mean a below-market price, but it comes with extra risk and effort. For most buyers, a Zillow pre-foreclosure is worth pursuing only with a knowledgeable agent and a clear budget for due diligence.

Is a Zillow Pre-Foreclosure Right for You?

A Zillow pre-foreclosure can be a genuine opportunity, but it rewards a specific kind of buyer: patient, prepared, and comfortable with uncertainty. If you need to be in a home by a fixed date, the unpredictable timeline of a Zillow pre-foreclosure may not fit. If you have flexibility, financing lined up, and an agent who knows distressed sales, the upside can be real equity on day one.

The smartest way to approach any Zillow pre-foreclosure is to treat the listing flag as a lead, not a deal. Verify the status, reach the owner, run your due diligence, and be ready to walk away if liens or repairs erase the discount. Buyers who stay disciplined come out ahead; buyers who fall in love with a Zillow pre-foreclosure before doing the homework usually don’t.

Bottom line: a Zillow pre-foreclosure is worth exploring if you understand it’s a negotiation with a distressed owner, not a click-to-buy listing. Go in with the right team and the right expectations, and it can be one of the better ways to buy below market.